Illumina (ticker: ILMN) experienced a significant sell-off in Q1 2025, driven by headwinds from the China ban, uncertainty around NIH funding, and rising competition. Given that these challenges emerged during Illumina’s director nomination window, it's not surprising that the sell-off attracted another activist, leading Illumina to appoint Keith Meister to the Board without a fight this time.

While Mr. Meister’s agenda will likely address these key issues, I believe resolving Illumina's corporate governance problems is just as - if not more - critical. Notably, Illumina is under SEC investigation over the Grail acquisition, which could prompt a Board overhaul as early as this year.

The investigation’s outcome may also have significant consequences, particularly in resolving the mystery of the “missing” 122.5 million Grail shares that should have been owned by Illumina. By my calculations, this amounts to an unresolved ~$1.4 billion issue. We still don’t know who received these financially valuable shares - or how.

Disclaimer:This newsletter is not investment advice. Views or opinions represented in this newsletter are personal and belong solely to the owner and do not represent those of companies that the owner may or may not be associated with in a professional capacity, unless explicitly stated.

Premium Newsletter

If you enjoy this write-up, consider subscribing to the Premium Newsletter.

Premium explores “real time” situations and looks for interesting governance signals before they potentially happen and/or gets priced in.

Activism! Part Deux

On March 25, 2025, Illumina announced activist Keith Meister is joining the Board with Chairman Stephen MacMillan resigning from the Board and Dr. Scott Gottlieb appointed the company’s next Chair, effective March 28, 2025.

While I believe Mr. Meister’s uncontested Board appointment was primarily catalyzed by the stock sell-off, I don’t think the same can be said about Mr. MacMillan’s resignation or Dr. Gottlieb’s appointment as Chair. I believe both of those decisions were highly informed - if not driven - by Illumina’s ongoing SEC investigation.

In my opinion, the SEC investigation is too material and consequential for Mr. Macmillan to reasonably step down from the Board before its resolution. It is also arguably the most critical Board-involved issue any successor Chair inherits, more so than the headwinds currently beating up the stock.

In particular, Keith Meister is inheriting an ongoing SEC investigation that I believe could lead to “material” consequences for the company, and he has the unavoidable responsibility of remediating this issue on behalf of Illumina shareholders.

The “Materiality” of the SEC Investigation

Since July 2023, Illumina has been dealing with an SEC investigation regarding the company’s August 2021 acquisition of Grail:

In July 2023, we were informed that the staff of the SEC was conducting an investigation relating to Illumina and was requesting documents and communications primarily related to Illumina’s acquisition of GRAIL and certain statements and disclosures concerning GRAIL, its products and its acquisition, and related to the conduct and compensation of certain members of Illumina and GRAIL management, among other things. Illumina is cooperating with the SEC in this investigation.

While Illumina hasn’t provided any updates to the SEC investigation, beyond their initial self-disclosure, I think it’s important to remember that voluntary self-disclosure is a “material” signal.

Typically, companies aren’t required to disclose the beginning of an investigation and can defer any disclosures until there’s more certainty of “materiality” (i.e. likelihood of enforcement action, settlement discussions, remediation efforts, etc.).

To self-disclose the start of a formal investigation is an indicator that the company believes the outcome of the investigation could be “material” to shareholders.

As for the “material” consequences Illumina potentially faces as part of this SEC investigation, I think it comes back to reconciling what happened to the undisclosed shares that seem to go “missing” from Illumina’s ownership after Grail raised their $120 million Series A round in January 2016.

The Grail Saga

As a reminder, many investors were puzzled by Illumina’s defiant re-acquisition of Grail in August 2021 - especially so soon after spinning off the company in January 2016 - and the substantial premium they paid in the process.

When I first explored this issue in Malignant Governance, I felt the heart of matter came down to undisclosed Grail shares and the possibility Illumina insiders (past and present) reaped a material, undisclosed financial windfall.

While company disclosures give the impression the financial windfall was limited, after sequencing (pun intended) the various Grail-related disclosures, Illumina shareholders need to consider the possibility the UNDISCLOSED financial windfall to insiders is well in excess of $500 million. And depending on your assumptions, that figure can conceivably be $1 billion+.

When Grail split-off from Illumina and raised its $120 million Series A round in January 2016 - of which Illumina contributed $40 million - Illumina’s equity ownership was diluted down from 100% to 52%. This didn’t make sense to me, especially given that Illumina also secured a long-term supply agreement with Grail, adding another 112.5 million Class B shares to its holdings.

At the time, to make the ownership math work (i.e. 52% fully diluted ownership, 90% common stock ownership), I estimated that up to 70 million Grail shares were allocated to “insiders” (i.e. employees, directors, and consultants) right from the start that were seemingly unaccounted for and undisclosed.

In retrospect, I may have underestimated the potential number of “missing” shares - crazy as that sounds.

Missing: 122.5 Million Grail Shares

When tracking Illumina’s ownership of Grail common stock (i.e. Class A and Class B shares) from the 112.5 million Class B shares received through the Illumina-Grail Supply Agreement in January 2016 onward, the numbers align with Illumina’s reported common ownership as disclosed in Grail’s S-1 filing on September 9, 2020.

In January 2016, GRAIL completed its Series A convertible preferred stock financing, raising $120.0 million, of which the Company invested $40.0 million. Additionally, the Company and GRAIL executed a long-term supply agreement in which the Company contributed certain perpetual licenses, employees, and discounted supply terms in exchange for 112.5 million shares of GRAIL’s Class B Common Stock.

(2) Consists of (i) 5,000,000 shares of Series A redeemable convertible preferred stock, (ii) 3,458,550 shares of Series B redeemable convertible preferred stock, (iii) 11,746,280 shares of Series D redeemable convertible preferred stock, and (iv) 78,105,879 shares of Class A common stock. Illumina, Inc. is a publicly-traded company.

The problem is that this common stock ownership count overlooks the 1,000 Class B shares issued to - and wholly owned by - Illumina when Grail was formed in September 2015.

These 1,000 shares may seem like a trivial rounding error until you consider that on January 8, 2016 - the same day Grail began selling Series A preferred stock - Grail amended its Articles of Incorporation to enact a 122,500-for-1 Class B stock split:

The GRAIL S-1/A of September 17, 2020 disclosed that Illumina received 1,000 shares of GRAIL’s Class B common shares in connection with GRAIL’s founding on September 11, 2015. The GRAIL Amended and Restated Certificate of Incorporation of GRAIL, Inc., as of January 8, 2016, disclosed that GRAIL had undertaken a share split whereby each holder of Class B common shares would receive 122,500 shares of Class B common stock for each share of such stock held on or before January 8, 2016.

Simply put, Illumina should have owned an additional 122.5 million Class B shares post-split that have gone “missing,” with no clear explanation of their whereabouts.

Undisclosed: 122,500-for-1 Stock Split

When you go through the SEC disclosures, both Illumina and Grail do not acknowledge the ownership or existence of these 122.5 million Class B shares.

This 122,500-for-1 stock split is completely undisclosed in the SEC filings and requires digging into Grail’s Delaware incorporation filings and amendments to find:

At the effective time of the filing of this Amended and Restated Certificate of Incorporation, and without further action on the part of the corporation or the holders of its stock, each share of Class B Common Stock of the corporation outstanding immediately prior thereto shall be split into One Hundred Twenty Two Thousand Five Hundred (122,500) fully paid and nonassessable shares of Class B Common Stock of the corporation, and at such time each holder of record of Class B Common Stock shall, without further action, be and become the holder of One Hundred Twenty Two Thousand Five Hundred (122,500) shares of Class B Common Stock for each share of Class B Common Stock held of record immediately prior thereto.

Source: Grail’s Amended Articles of Incorporation (filed on January 8, 2016)

Furthermore, we have no idea who received these 122.5 million Class B shares from Illumina, nor is there any explanation for their absence from Illumina’s share holdings after the Series A round - to reconcile with its 90% common and 52% fully diluted ownership.

Resolving Illumina’s ~$1.4 Billion Problem

When Carl Icahn was involved at Illumina, the Grail-related issues were allegedly egregious enough for Mr. Icahn to file his own lawsuit against the company.

It would be a great mistake to allow the legacy conflicted directors to influence Illumina given their history of reckless decision making and value destruction. When we say conflicted, we mean that directors that are worried about personal liability for the billions of dollars they have cost the Company through their negligence cannot be trusted to make clear minded decisions.

These “legacy conflicted directors” remain on Illumina’s Board, and I believe Keith Meister has a responsibility to address the corporate governance issues they allegedly contributed to.

In my view, one of the most pressing issues for Mr. Meister as Illumina’s newest director is resolving what happened to the company’s 122.5 million “missing” Grail shares. Based on my calculations, these shares account for ~$1.4 billion of Illumina’s $9.8 billion purchase price for Grail. I believe this ~$1.4 billion “problem” is likely at the heart of the SEC investigation.

There aren’t many ways for such a massive number of shares - 122.5 million - to simply “disappear” without proper disclosure, and I suspect much of it involves fraud by omission.

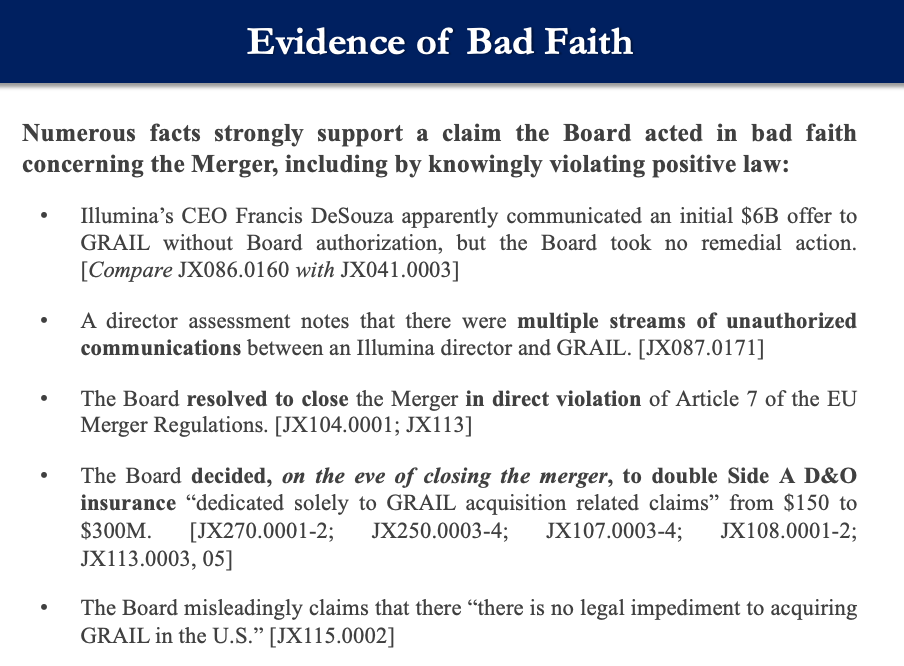

Moreover, based on Illumina board documents reviewed by plaintiffs in various shareholder lawsuits, this ~$1.4 billion “problem” is compounded by Illumina’s “bad faith” pursuit of Grail:

Source: Pavers and Road Builders Section 220 Trial Argument (filed on June 11, 2024)

As a result, I don’t believe Illumina’s Board overhaul is complete. Mr. Meister will likely play a key role in driving further changes, with the SEC investigation providing him significant leverage, and it wouldn’t surprise me if there’s an announced resolution and/or settlement to the SEC investigation this year.