Twitter: Corp Governance "Dark Arts" (Part 6)

Elon’s whirlwind April 2022 pursuit of Twitter through the lens of "dark arts"

Welcome to Nongaap Newsletter! This write-up was first sent to premium subscribers and later unlocked.

I’m Mike, an ex-activist investor who writes about corporate governance, the power & friction of incentives, strategy, interpersonal board dynamics, activist fights, and other random topics.

Corporate Governance “Dark Arts” Series

After a 2 year hiatus, I’m back with Part 6 of the Corporate Governance “Dark Arts” series.

Through explainers and case studies, this series examines how insiders use the “Dark Arts” of corporate governance to take advantage of unsuspecting stakeholders, influence decision-making, profit, etc. And yes, there can be windows of opportunity to participate alongside.

Part 6: Elon Musk’s April 2022 Pursuit of Twitter

NOTE: Since the deal isn’t closed yet (as of October 25, 2022), I’m going to keep this write-up behind a premium paywall and will unlock to Free subscribers on October 29, 2022 after the expected close date of October 28, 2022. Update (as of October 27, 2022): Deal closed so unlocking post.

For Part 6, I’m covering Twitter (ticker: TWTR) and Elon Musk’s whirlwind April 2022 pursuit to acquire Twitter for $54.20. There’s already been plenty of coverage on this deal, but hopefully I can squeeze a couple more drops of governance-based insight for you.

This write-up will primarily focus on the puts-and-takes of RSUs granted to executives on April 13, 2022, the same day Elon Musk submitted a non-binding proposal to the Board to acquire Twitter for $54.20, and one day before he disclosed that offer to the public.

It appears to be a spring-load, but requires a bit more unpacking to really understand what’s going on and how it’s still potentially a useful signal after Elon Musk publicly disclosed his offer. As a reminder, “spring loading” is when equity is granted before positive MNPI is released that positively impacts the stock price.

In this particular case, Twitter RSU grants appear to be spring-loaded, but the price impact of Elon Musk’s offer is arguably all over the place (i.e. swinging from muted to volatile depending on incremental news flow) due to Elon Musk’s own (inadvertent?) “dark arts” activities and the general “center of gravity” he has in the market.

Let’s dive in.

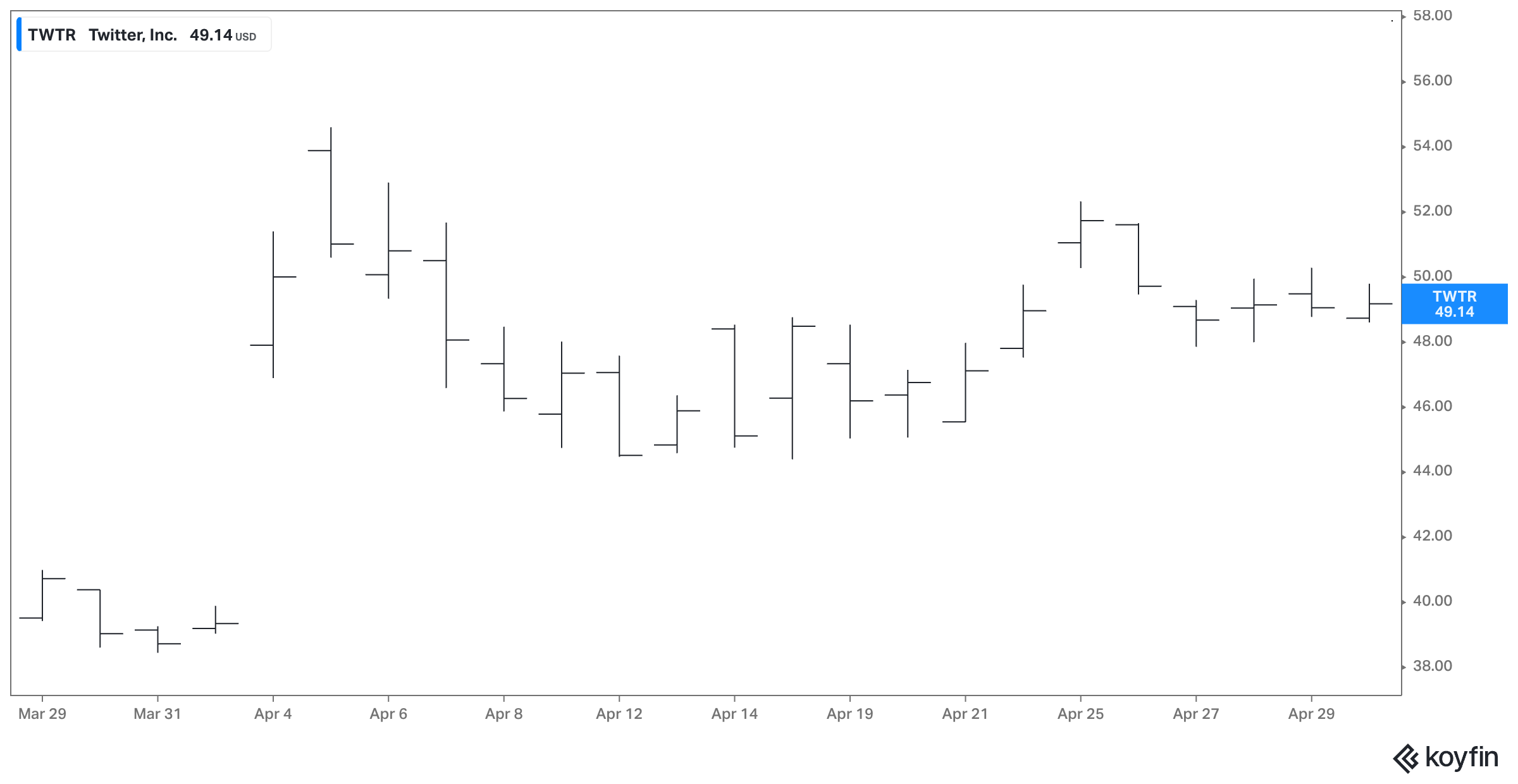

Window of Opportunity: Volatile Post-Offer Price Action

April 2022 was a whirlwind month for Twitter (and its stock) thanks to Elon Musk.

When examining the volatile price action following Elon’s offer, I think it’s fair to say the spread between Twitter’s stock price and Elon’s $54.20 offer was wide-ish (~15% to 20%):

That’s not to say the spread was irrational. If the offer wasn’t accepted and Elon Musk blew out the stock, you’re looking at a 15% to 20%+ reversal to the downside.

With the luxury of hindsight, we know there was a “window of opportunity” to capitalize on price volatility to accumulate shares prior to a deal announcement. Now, without hindsight, putting on a “risk adjusted” ex-ante bet requires answering/addressing a few key questions:

Is Elon’s bid for real?

Can Elon finance the deal?

Will Twitter seriously consider the offer and accept it? Or will they fight?

Does ongoing market weakness cause Elon to pull the offer?

While it be nice to have an army of lawyers, bankers, analysts, and rolodex contacts to help answer/address these questions, I’m primarily using public SEC filings, a Twitter account, Google search, and [accepting sponsors] subscription.

Luckily, corporate governance knowledge can help us a lot and I’d argue we can leverage “dark arts” signals to meaningfully answer/address these questions and help us identify a “risk adjusted” ex-ante trade.

Ex-Ante Thesis: Twitter Will Accept Elon’s Offer

Before I jump into my ex-ante thesis, let’s layout a timeline of key events:

April 4: Elon Musk discloses 9.2% stake and the stock pops 27% to $49.97.

April 5: Twitter announces Elon Musk will join the Board.

April 11: Actually, Elon Musk won’t join the Board.

April 14: Elon Musk offers to buy Twitter for $54.20.

April 15: Twitter adopts poison pill.

April 21: Elon Musk discloses commitment letters to finance the deal

April 25: Twitter accepts Elon Musk’s offer

With this timeline in mind, I’m going to share some personal notes from April 15, 2022 (source: trust me bro) that lays out my “dark arts” ex-ante thesis that Twitter will accept Elon’s offer and/or seriously evaluate strategic alternatives.

Some of this might not makes sense if you’re not familiar with “dark arts” concepts, but I’ll try to unpack/explain key takeaways in subsequent sections:

[Overly edited for clarity and to heighten dramatic effect]

April 15, 2022

Dear Diary,

RSUs granted to management on April 13, 2022 is a tell!

April 13th is on the same day Elon privately sent an offer letter to the Board to acquire Twitter for $54.20 and 1-day prior to Elon publicly announcing the offer.

Keep in mind, this offer comes off the heels of Elon joining - and then not joining - Twitter’s Board earlier in the month. It’s hard to know what exactly happened for him to reverse his decision to join the Board, but this offer leads me to believe he wants to move fast on making a deal happen and doesn’t want to be locked-up with a Board.

There’s certainly added risk he’ll blow out the stock if Twitter doesn’t accept the offer, but I suspect the announced poison pill signals he’s pot committed and willing to keep buying if there isn’t a guardrail put in place.

I actually wouldn’t dismiss the idea Elon threatened to accumulate more shares to acquire Twitter in conjunction with abruptly declining the Board seat offered to him. After all, he wasn't exactly playing by the book by accumulating ~9% of the company without proper disclosures…

As for the recent equity grants to management, it feels like they’re materially shifting equity to RSUs (or simply loading up on it) to maximize risk-adjusted value if a deal is done while managing downside if Elon pulls out. The mix shift in equity compensation also seems to imply Elon communicated an intent offer days ago (when he declined the Board seat? when he started to buy?), because it appears the Board had time to make adjustments to equity compensation.

Overall, these RSU grants feel very intentional and specific to driving/managing a sale of the company. Also, combined with last year’s VCA grant that doesn’t start to vest until the stock is $100 per share, but will vest upon a change-in-control termination (regardless of takeout price), there’s a lot of temptation and incentive for management to accept Elon’s offer.

Might want to consider an event-driven trade if the spread looks compelling.

So when you review the key questions in the previous section through the lens of corporate governance “dark arts”, you get some useful answers/speculations:

Is Elon’s bid for real?

Board was signaling the bid was “real” enough to prioritize RSUs.

Can Elon finance the deal?

Hard to say, but I don’t think the sizable RSU grants happen without some belief he can finance the deal. Alternatively, RSUs offer a better “floor” in value if a deal falls through due to financing issues.

Will Twitter seriously consider the offer and accept? Or fight?

They’re going to seriously consider the offer and are signaling they’re much more likely to accept a takeout offer than fight to stay public. The RSUs are, in my opinion, geared towards doing a deal.

Does ongoing market weakness cause Elon to pull the offer?

It’s the biggest risk factor, but he’s prone to move fast and sort out the consequences later. Shifting to RSUs potentially signals the Board and management is also willing to move fast to lock in a deal.

All things considered, I felt the RSUs were telling me Twitter wasn’t going to fight the offer and were incentivizing the team to get a deal done expeditiously (I thought within ~4 weeks).

“Dark Arts” Signal: Equity Compensation

I know I just threw a lot at you so let’s try to unpack the signals derived from the April 13, 2022 RSU grants.

For this section, I’m going to use Ned Segal’s grant of 221,730 RSUs as an example:

221,730 shares X $45.85 grant date price = $10,166,321

That’s a nicely sized grant!

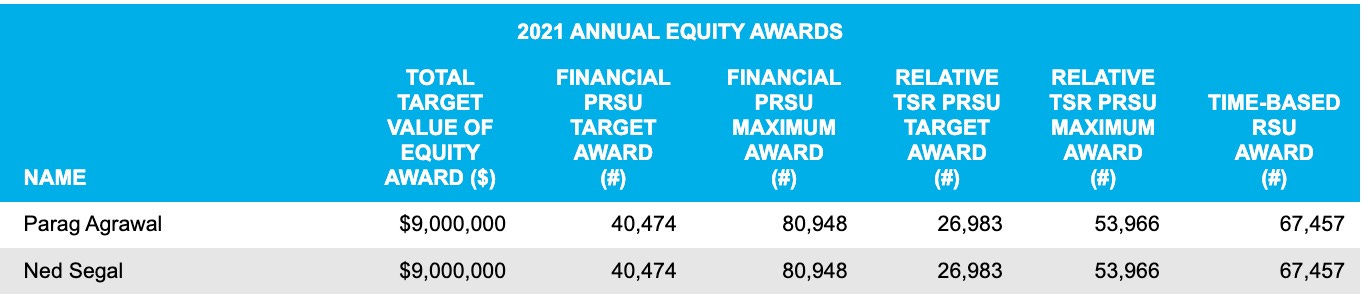

For reference, Ned Segal’s target 2021 annual equity compensation was $9 million, split 50-50 between PRSUs and RSUs:

So either:

Ned’s equity compensation shifted to 100% RSUs in 2022, or

Ned was given a massive grant (i.e. $20m in total equity value) if the 50-50 split remains the same.

Companies don’t disclose PSUs in the form 4 so we don’t know for certain which one it is, but I can say this grant size cannot be ignored considering Ned Segal had 214,221 unvested RSUs in aggregate per the 2022 Proxy. Twitter basically doubled his unvested RSUs by granting him 221,730 RSUs on April 13, 2022 and around the same time the Board was aware Elon Musk was going to make an offer to acquire the company.

The potential “signal” here is the grant is being informed by the likelihood strategic alternatives (i.e. Elon’s offer) will be happening in earnest, and the equity mix is “accommodating” that process. RSUs tend to be a “cleaner” equity instrument to grant in case of sale happens and generally removes any unexpected complications or setbacks (i.e. performance vesting conditions, etc.).

Also, Ned’s sizable 2022 RSU grant, combined with 241,508 “value creation” RSUs ($15m target grant value) he received off-cycle in July 2021, creates a massive incentive to accept Elon’s offer due to generous change-in-control termination accelerated vesting (more on that later) versus staying-the-course.

You have to assume the Board is aware of that “massive incentive” when they approved the grant, and that can be a pretty important signal.

Overall, Twitter’s Board is materially tilting incentives towards doing a transaction by granting sizable RSUs to management on April 13, 2022. If the Board and management thought the company offered tremendous long-term value and wanted to incentivize management to stay the course as a public company, you’d probably see a greater mix of options and/or PSUs which can pay 200% hitting max targets vs. granting an inordinate amount of RSUs.

“Dark Arts” Signal: Accelerated Vesting

How unvested shares accelerate vest upon a change-in-control termination is a really important signal to monitor. Twitter, in my opinion, has a generous accelerated vesting policy (i.e. CEO and CFO getting 100% accelerated vesting) for termination upon change in control.

Generous vesting can distort decision-making and push management teams to pursue deals that will vest shares that have no business vesting and should be forfeited.

For example, in July 2021, management received “value creation” RSUs that required hitting the following stock prices over 4.5 years to vest:

Those are really tough hurdles, especially after the stock sold off hard to the $30s earlier this year. The issue is these price hurdles don’t matter in a change-in-control termination, and will accelerate vest without any consideration to the stock price.

This creates massive incentive to accept Elon’s $54.20 offer.

For instance, CFO Ned Segal would effectively get a $13m “bonus” selling the company and triggering change-in-control termination accelerated vesting on his 241,508 “value creation” RSUs that are unlikely to 100% vest otherwise.

Ex-Post Review: Background of the Merger

The best part of corporate governance research (especially “dark arts”) are the feedback loops. You learn pretty quickly whether or not your thesis is correct and can iterate on your learnings.

I highly suggest reading the background of the merger for yourself, but it’s pretty clear Elon Musk told Twitter on multiple occasions - going back to March - he was considering acquiring the company, and Twitter’s Board was taking those gestures seriously retaining advisors, discussing potential outcomes, etc.:

On March 27, 2022, Messrs. Musk, Taylor and Agrawal discussed Mr. Musk’s interest in Twitter and potentially joining the Twitter Board. As part of that discussion, Mr. Musk stated that he was considering various options with respect to his ownership, including potentially joining the Twitter Board, seeking to take Twitter private or starting a competitor to Twitter.

On March 31, 2022, Messrs. Agrawal and Taylor met with Mr. Musk to discuss Twitter’s business and Mr. Musk’s potential interest in joining the Twitter Board. At the meeting, Mr. Musk reiterated his interest in potentially joining the Twitter Board to help improve Twitter’s business as a director of Twitter, and that he was also considering the possibility of taking Twitter private or starting a competitor to Twitter.

On April 9, 2022, before Mr. Musk’s appointment to the Twitter Board became effective, Mr. Musk notified Messrs. Taylor and Agrawal that he would not be joining the Twitter Board and would be making an offer to take Twitter private. Mr. Agrawal informed the members of the Twitter Board of Mr. Musk’s communication.

April 10, 2022, at Mr. Taylor’s direction, Twitter requested that Goldman Sachs attend meetings of the Twitter Board to assist in Twitter’s evaluation of a potential acquisition proposal from Mr. Musk and related matters.

On April 13, 2022, Mr. Musk delivered to Mr. Taylor a non-binding proposal to acquire Twitter

Musk also signaled a desire to overhaul leadership and that likely played a role in declining a Board seat and pursuing an outright acquisition.

After connecting some dots, the sizable RSU grants make more sense and the “dark arts” signals are validated now that you know Elon Musk was in communication with Twitter for weeks leading up to his April 13 offer letter and was keen to clean house. That dynamic certainly informs the April 13, 2022 equity grants, and why management would be inclined to pursue a deal and then accelerate vest upon termination.

Overall, what makes the April 2022 RSU grants so interesting to me is you’re still able to leverage signal after the acquisition offer is made by Elon Musk.

Dark Knight vs. Dark Elon

To wrap up, I don’t necessarily begrudge Twitter for granting the RSUs the way they probably did. This isn’t an easy situation to manage given all the moving parts and the way Elon Musk accumulated 9% without disclosure, pops the stock 27% ahead of annual equity grants, is actively interested in acquiring the entire company, and wants to clean house.

This was basically a Dark Knight vs. Dark Elon type storyline playing out with the Board implementing “Dark Arts” to White Knight a friendly outcome for management as they dealt with an activist shareholder who was also using “Dark Arts” to accumulate a highly influential and dominating position without proper disclosures.

Speaking of proper disclosures, one thing I’m kind of curious about is how these grants were expensed and accounted for by Twitter if they are indeed spring-loaded grants.

The SEC has made spring-loading a priority and is pushing for appropriate accounting and disclosures:

"It is important that companies' accounting and disclosures reflect the economics and terms of these compensation arrangements," SEC Chair Gary Gensler said. "This gets to the SEC's remit to protect investors." (SEC Press Release)

The staff reminds companies of the importance of strong corporate governance and controls in granting share options, as well as the requirements to maintain effective internal control over financial reporting and disclosure controls and procedures. (SAB 120)

Not to toss a molotov cocktail, but has Elon Musk attempted to get out of this deal by accusing Twitter of failing to maintain “effective internal control over financial reporting and disclosure controls and procedures” and not appropriately accounting for and disclosing these allegedly spring-loaded grants?

I kid, I kid.

I get it now. Great call. If published earlier you could be talking yout TWTR victory lap as others are ..over and over...after being on right side of that trade. The illegal shit going on in pain site is nuts. Everyone was all over Musk for not disclosing the 9% yet not a word on this.

Mike, love your work.

One question tho, if TWTR did not disclose the 4/22 RSU how do we know about them?